Silicon Valley: A Global Epicenter of Technological Innovation and Growth

Exploring the Factors that influence Silicon Valley's Dominance in the Tech Industry

Thriving Innovation Hub: Silicon Valley fosters disruptive startups in AI, biotech, cloud computing, and more, sustaining its reputation as an innovation epicenter.

Robust Ecosystem: Key elements include venture capital, human capital, university ties, government support, industrial structure, and professional services network.

Unicorn Dominance: With 285 unicorns valued at $1,053.74 billion, Silicon Valley's startup ecosystem remains globally unparalleled in value and impact.

Oversaturation and startup exodus: While an increasing number of startups leave Silicon Valley due to exorbitant costs, Silicon Valley is also reaching oversaturation with growth rates falling behind global averages.

With top companies like Apple, Google, Microsoft, Salesforce, Tesla, and Meta founded and raised in Silicon Valley, the ecosystem has seen everything right from inception to the advanced commercialisation of these startups into large corporate structures that is required as growth reaches a certain threshold. Now that these companies have evolved and gone public, they no longer qualify as startups. Yet, the innovation ethos that has been inculcated in Silicon Valley since the get go still rings around, ensuring that the valley continues to foster new generations of disruptive startups as technology booms and matures.

So, SV finds itself even today as the hub of activities enabled by the internet, cloud computing, social media, smartphones, the Internet of Things, artificial intelligence (AI), and climate-related technologies, even as it also was home to a robust biotech industry. And we can clearly see this in OpenAI, the AI brainchild of visionary founder Sam Altman. OpenAI launched the disruptive open source Large Language Model, ChatGPT, and is today valued at $80Bn, with investments and partnerships with Microsoft, Tiger Global, Sequoia, Amazon, Infosys, among others.

As per Startup Blink, Silicon Valley is home to 11,811 startups, representing ~20% of all US startups. The significantly larger ecosystem value of $2.5Tn as compared to the global average ecosystem value of $29.4Bn, brings down the growth rate significantly. The SV ecosystem grows at only 10% ( For companies founded in H2 2021 - H2 2023 VS companies founded in H2 2019 - H2 2021) as compared to the global average of 46%. This is seen as a result of the apparent oversaturation seen in the ecosystem.

Broadly speaking, the Silicon Valley ecosystem can be distilled into its primary components: (1) venture capital, (2) human capital, (3) university-industry ties, (4) direct and indirect government support, (5) industrial structure, and (6) support ecosystem of professional service firms. What started as a innovation centre for defence technology, Silicon Valley reinvented itself through multiple iterations of which some are semiconductors, personal computers, smartphones, modern software, and today’s emerging trends, which include but are not limited to - Artificial Intelligence and Machine Learning, Spatial Computing, Edge Computing, biotech developments in gene editing and other fields, and Quantum Computing.

Today, some tech companies in Silicon Valley are having second thoughts about abandoning their offices and letting everyone work from home now that lockdown restrictions are easing. Companies like Google have requested employees slowly come back to the office, while others, like Spotify, have let their workers set up offices anywhere in the world. An emergent trend in Silicon Valley is the rise of the concept of the global workforce, where employees can be from anywhere around the world, connected through the same technology that connected people during the pandemic. This technology also finds itself on a path of continual innovation leveraging on telepresence robots and Virtual Reality. This allows SV startups to hire top talent from all around the world, without them having to relocate, and without the startup having to go through the regulatory and administrative hassles of having more foreign workers.

Funding and Unicorns

2022 and 2023 saw a free flow of investor capital into Artificial Intelligence startups, what many call a looming AI bubble. This free flow unfortunately created a capital drought for other startups. According to early PitchBook data (Jan 4), venture capitalists invested $170.6Bn in the US in 2023, over an estimated roughly 15,000 deals. That deal value is down by about 30% from 2022.

And not just in the US, VC took a hit globally, with investments down 35% from 2022 and the lowest outlay since 2017. But this scarcity is not restricted to the pockets of startups but also the investors themselves. Money raised by US venture investors declined by almost two-thirds from 2022, and by almost half globally.

While this affected startups worldwide in terms of capital availability, it was in some senses a destined outcome, considering the 2021 investments bubble. Inflated valuations, decelerating IPO activity, and a concern of sacrificing satisfactory performance metrics of the likes of IRR, TVPI, DPI, and RVPI induced a subsequent bubble burst in 2022 which dragged on to 2023. This is a link to an article which explains this.

However, as we can see in this figure, while the San Francisco Bay Area was responsible partially for the VC funding boom of 2020 and 2021, the bulk of this overexertion was carried out by external players in the US since VC funding in SF Bay Area actually saw a dip as a percentage of total US VC investments in 2020 and 2021 as compared to previous years. This shows some potential for rational investment strengthening in the area.

As for the stage breakdown of investments into the US, early stages, pre seed investment was $783Mn, $5Bn for pre-series A, $20Bn for Series A, $26Bn for Series B, $27Bn for Series C, and $79Bn for later stages. These stages saw varying growth rates, with early stages showing a fall of 31% funding from Q4 2022 - Q1 2023 to Q4 2023 - Q1 2024, mid-stage showing a fall of 20.3%, and late stages showing a fall of only 12.2% in the same period. This shows how most of the burden of the funding shortfall was borne by early stage founders and startups.

Now to put things into context, as per CrunchBase, the world has 1,229 Unicorns as of March 20, 2024, at a combined valuation of $3,846.11Bn. Out of these, the US has 656 Unicorns at a combined valuation of $2,111.70Bn. Core Silicon Valley (made up of San Jose, Palo Alto, Sunnyvale, Mountain View, and others) makes up 95 unicorns out of this, totalling at a $240.36Bn. However if you were to consider a broader definition of Silicon Valley, to which it has extended practically speaking, it includes San Francisco, Newark, Fremont, Hayward, Berkeley, and Oakland which along with Silicon Valley is collectively known as the San Francisco Bay Area or simply Silicon Valley. Now this Silicon Valley together hosts 285 unicorns with a combined valuation at $1,053.74Bn. This means that Silicon Valley, with a combined population of less than 4 million people, contributes to about 27.4% valuation of unicorns globally and about 49.9% of US unicorns in valuation.

The bulk of this mammoth valuation is driven by a few large players which has been the nature of Venture Capital since times remember. SF Bay Area hosts 21 Decacorns with a valuation of $426.09Bn. Most valuable startups are OpenAI ($80Bn), Stripe ($65Bn), DataBricks ($43Bn), Chime ($25Bn), Miro ($17.5Bn), Anthropic AI ($16.05Bn). Along with them, one of the big success stories of Silicon Valley is Navan, formerly TripActions, which offers an integrated Business Travel & Expense solution. It is valued at $9.2Bn and is headquartered in the intellectual centre of Silicon Valley - Palo Alto. Founded in 2015, Navan is now planning to IPO in 2024, as well as hit profitability. Navan has been able to reach its present state because of the significant tailwind the favourable funding environment of Silicon Valley provided. It raised $2.2Bn from marquee investors like a16z, Lightspeed, Zeev, Greenoaks, and others. Moreover, the founding DNA of this company is sourced from former executives of none other than the kickstarter of Silicon Valley itself - HP.

Yet, it is quintessential to consider how funds being at founders’ fingertips affect the ecosystem and more importantly, the startups. It has been conventionally believed that greater access to capital creates greater growth. Not necessarily. A recent article by TechCrunch brought to light how better funded companies were found to not be actually better performers as compared to less funded companies, with the exception of a few critical extreme outliers. Moreover, these companies went on to be worse performers after IPOs. This brings to the surface a concept known as efficient entrepreneurship, which raises concerns over the funding frenzies most founders find themselves in at the sight of small successes. Point is, while Silicon Valley does act as a hub of startup investments, being the breeding ground for today’s refined VC industry, overinvestment may not be a good thing, which might bring down VC returns overall in the long term. However, corrections like the 2023 correction show that despite certain effervescent years, calm and balance generally takes over.

Investments and Key Investors

Silicon Valley, being one of the oldest and most well-established startup ecosystems in the world, hosts multiple mega-VCs, Corporate VCs (CVCs), corporates themselves, and smaller VCs specialising in niche sectors and geographies. For instance, in January 2023, Microsoft, which is also based in the area, invested $10Bn in OpenAI. Microsoft benefits from the large applicability of OpenAI in various Microsoft use-cases, the clearest one being its search engines.

With the introduction of the world-renowned LLM model released by OpenAI in November 2022, AI investments picked up rapid pace. Even today, that pace is accelerating, with AI VC funding standing at $19.5Bn in 2024 first quarter as compared to 2023 Q1. xAI is an Artificial Intelligence research and development company founded by Tesla founder - Elon Musk. Today, xAI seeks $6Bn in funding from key venture capital firms in Silicon Valley like Andreessen Horowitz, Sequoia Capital, and Tribe Capital, valuing it at $18Bn. Inflection AI is another artificial intelligence studio, which has developed the world’s first personalised artificial intelligence LLM. It has raised $1.5Bn in funding over two rounds, with a recent $1.3Bn round in June 2023.

Now, when we say key VCs, what do we mean? These are VC firms that have played a pivotal role in the development of Silicon Valley into what it has become today. Some of them are -

Bessemer Venture Partners - One of the earliest VC firms in SV, it has made 1,364 investments to date with 301 successful exits (145 IPOs), ranging across various sectors and all stages, and boasts success stories such as LinkedIn, Pinterest, and Shopify.

Accel Partners- Having made over 2,000 investments across technology sectors, and all stages, Accel holds a vast portfolio with 367 exits and winners like Spotify, Slack, Facebook, etc.

Andreessen Horowitz - With a significant share of tech founders as GPs, a16z prefers investments in technology and social media, with 1,474 investments, 210 exits, and names like Lyft, Coinbase, Pinterest in its arsenal.

Sequoia Capital - Being industry agnostic, Sequoia has been investing in early and growth stages, making 1,886 investments with 376 exits and has spawned behemoths like Google, Apple, and PayPal.

Kleiner Perkins - Creating successes such as Google, Amazon, and Uber, Kleiner Perkins has made 1,397 investments and 335 exits. They are sector and stage agnostic.

The list goes on. Other marquee players are Khosla Ventures, Index Ventures, First round Capital, Menlo Ventures, Benchmark Capital, Matrix Partners, Bain Capital Ventures, New Enterprise Associates, Lightspeed Ventures, Greylock Partners, True Ventures, Google Ventures (CVC), Venrock Associates, Redpoint Ventures, Canaan Partners and others.

Support Structures and Catalysts

Silicon Valley was the birthplace of Y-Combinator, which is globally recognised as the initiator of the accelerator model as known today. Incubators and accelerators provide startups with access to funding, mentoring, education, networking, resources, structure, and visibility, all of which together create both pre and post exit opportunities for rapid growth and success. Y Combinator, known as YC, birthed success stories like Reddit, Stripe, Airbnb, Cruise, DoorDash, InstaCart, all leading household names and more importantly success stories in the space of entrepreneurship. Similarly, 500 Startups, Founder Institute, Women’s Startup Lab, Prospect Silicon Valley, BetterLabs, World Innovation Lab, and others create significant collaborative and structural value for their startups and portfolio companies, with a focus towards rapid growth through direct action, compared to traditional VCs, which mostly provide value externally and through capital.

Not just for local startups, Silicon Valley is emerging as a hub for global innovators to set shop. In November 2023, Japan’s Ministry of Economy, Trade, and Industry (METI) opened the Japan Innovation Centre, a base to support global scaling of Japanese startups. This was followed by an announcement by the non-profit entrepreneurship organisation TiE Silicon Valley which talked about how they will train, mentor, and facilitate Indian startups to expand their presence in the US. January 2024 saw Philippines government and industry representatives launching a strategy to develop Philippines startups in Silicon Valley. These developments create an optimistic outlook for Silicon Valley as a global hub for global startups, unlimited by geography. Similarly, ICON SV acts as a bridgeway for Israeli startups to establish a base in Silicon Valley.

As far as the Government is concerned, it has been one of the major forces behind not only the growth but also the origination of Silicon Valley. The vast majority of integrated circuits sold in the early 1960s were for defense and space systems purchased by the government. Today, with a burgeoning defense budget of $850Bn, the government focuses on integrating technology into defense, to not only drive efficiency but stay ahead in the uncertainty brought on by the emerging cold war. Understandably, Silicon Valley leads the U.S. Defense Tech, with Congress allocating $111Mn to the Defense Innovation Unit, a Silicon Valley-based organization dedicated to accelerating the adoption of technology throughout the military. This creates further inroads for future policy support for startups with government collaboration in the area. Another factor of growth that has helped SV is that California has long prohibited employers from entering agreements to prevent their employees from leaving to compete against them.

Other ‘co-founders’ of Silicon Valley have been anchor Universities - Stanford and University of California Berkeley. These universities birthed multiple successful startups over the years, created either through university research or as a result of the talented graduates generated by these universities. These startups led to huge companies, which led the founders to give back to their university through support and donations, which helped the universities accumulate experience and expertise in industry-university collaborations, facilitating subsequent rounds of university-industry collaboration and spinouts. More importantly, the quality of education and ancillary support infrastructure induced an inflow of talented individuals from all around the world, who were further motivated by the ecosystem developing in the area, to move to SV. This allows startups to access this high-quality global talent at their fingertips. This is exactly why Stanford and UC Berkeley rank first and second in terms of number of founders produced by them standing at 1,435 and 1,433 respectively.

Technology and Innovation Economy

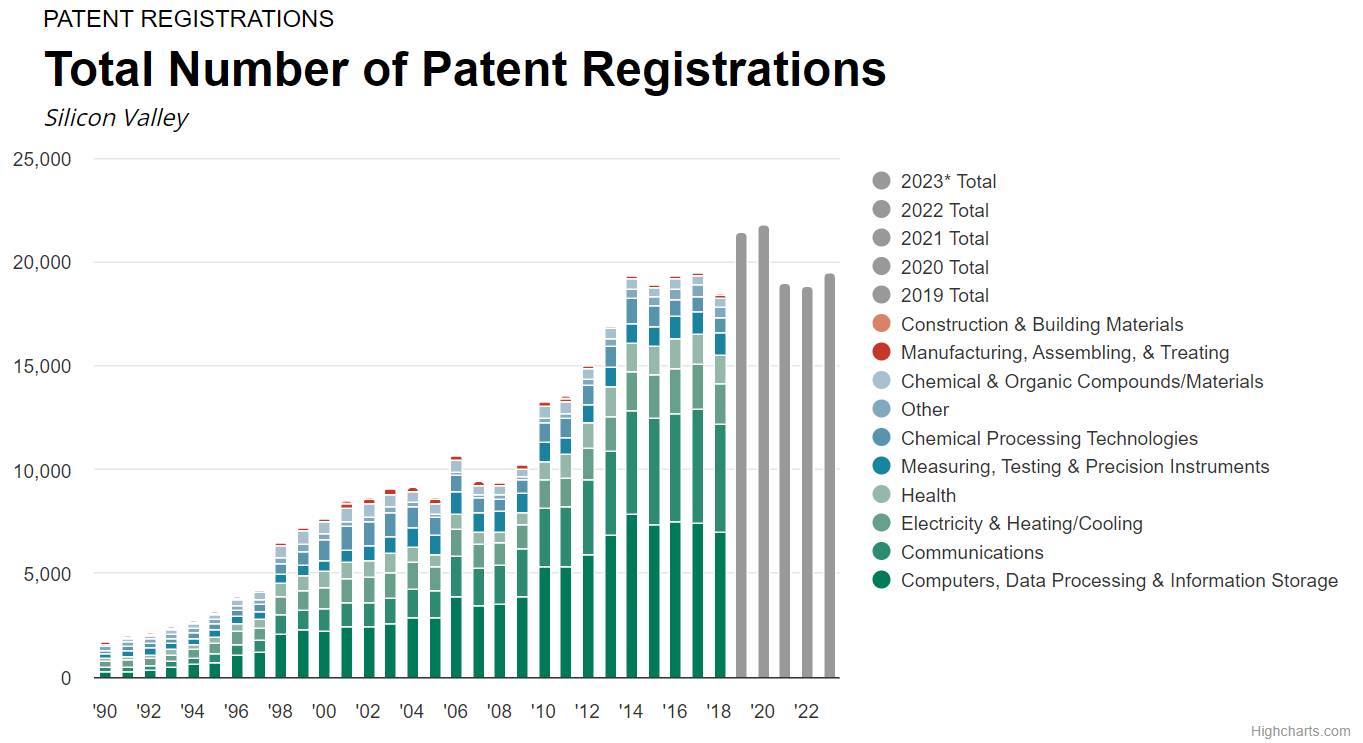

Silicon Valley has seen a phenomenal rise in the number of patents produced from about 2,000 patents in 1990 to about 19,500 patents in 2023, at a CAGR of 7.15%.

Within California, SIlicon Valley produces about 541 patent registrations per 100,000 people, while California average is 111 patents per 100,000 people, while US average for large metropolitans is 40. Out of the top 15 cities in terms of number of patents in the United States, 8 are a part of Silicon Valley, with a combined contribution of 11.5% of United States patents.This shows two important highlights about Silicon Valley - (1) The innovation ecosystem is robust, with a larger component of the populace applying and securing patents for their innovations and inventions, and (2) The regulatory infrastructure is supportive and catalyses innovation by providing Intellectual Property protection through effective patent provision.

When it comes to technology, Silicon Valley is the first name that comes to mind. And even today, in the ever-changing world of technology, Silicon Valley remains at the forefront. Some of the key trends redefining technology in SV are -

Artificial Intelligence - This does not seem out of place considering the interest the world has suddenly gained in this field. Not simply from software giants like OpenAI, but this growth is also going to be defined by hardware players. Nvidia for instance has created an impregnable hold over the AI chips industry, by recognising the trend early on and developing key pieces of software and hardware for the same. Now, seeing the immense growth potential in this space, new startups like MatX are bringing back chip manufacturing to Silicon Valley. They are creating chips specifically for Large Language Models, fuelled by their recent raise of $25Mn.

Spatial Computing - Spatial computing is a technology defined by computers blending data from the world around them in a natural way. With an ever-increasing adoption of technologies like Virtual Reality, Internet of Things(IoT) sensors, digital twins, Augmented Reality, and other forms, Spatial Computing is taking an upward turn, with a strong focus from leading companies like Apple with their recent Apple Vision Pro.

Quantum Computing - Simply put, Quantum computing utilizes quantum mechanics to solve complex problems faster than on classical computers. This proposes various use cases such as simulating chemical systems for faster drug discovery, or analysing and optimising financial portfolios. Today, PsiQuantum, a SV quantum computing startup seeks to build a error-correcting utility-scale quantum computer by 2027, using photonic-based architecture. The firm also raised a new $620Mn fund from the Australian Government to build its quantum computer.

Moving on to open source projects, Silicon Valley yet again emerges as one of the hub locations for such revolutionary models. Python, Linux, GitLab, GutHub, Redhat and others have displayed the vast utility that such models pose to the community and the company themselves. Today, Commercial Open Source Software (COSS) is gaining popularity as a profitable and sustainable business model. OpenAI and other open source softwares are creating further excitement in AI COSS. And they also tend to be more efficient in terms of capital.

Competitive Landscape

The Global Startup Ecosystem Report, published by StartupGenome acts as the best and most comprehensive resource available on startup ecosystems. It factors in soft and hard influences from financing to connectedness. In 2023, Silicon Valley ranks the first, followed by New York and London at #2, which has been the case since 2020. Los Angeles stands at #4 and Tel Aviv at #5. These are followed by Boston, Beijing, Singapore, Shanghai and Seattle. Singapore has made significant inroads in 2023, moving up 10 ranks from #18. From India, Bengaluru stands at #20, Delhi at #24, and Mumbai at #31.

Overall, Indian ecosystems have been moving up on the ranking while Chinese ecosystems have been going down due to stricter regulations, lingering impact of tenacious COVID-19 restrictions, and decreased availability of funding recently in China. Apart from top ecosystems, some emergent ecosystems to look out for in upcoming years will be Dubai, Indonesia, India, Seoul, Berlin, Tokyo, Paris, Stockholm and others. Overall, while Asia is seeing a stronger boost by the government, cultural concerns, lower risk appetites, and revenue-focused investors might deter future growth.

London remains Europe’s premier startup ecosystem. The region has seen an upswing in exits over $50 million, with several high-value exits over $1 billion, including Wise ($12.2 billion). In addition, Europe's largest Fintech unicorn, Revolut, is based in London, boasting a valuation of $33 billion. VCs invested $12 billion in London in 2023. UK’s Financial Conduct Authority seeks to simplify listing regulations and the Advanced Research and Invention Agency seeks to spawn innovation in new technological fields.

New York City has witnessed a 42% increase in exits above $1 billion since the GSER 2022, including Healthtech Roivant’s Q2 2021 $7.3 billion exit, and now boasts 126 unicorns. Digital asset exchange Gemini is its highest-valued tech unicorn at $7.1 billion, contributing significantly to the 71% increase in Ecosystem Value from 2019H2 - 2021H2 to 2020H2 - 2022H2. 25,000 tech-enabled startups supported by over 200 coworking spaces and 100 accelerators and incubators. Meanswhile NYC’s $80 million CS4All initiatives and the CUNY 2X tech program seek to enhance the tech talent pool in NYC.

Los Angeles saw a 29% increase in exits over $50 million and an impressive 110% increase in exits over $1 billion, GoodRx’s $12.7 billion valued IPO being the top exit. The number of LA unicorns has increased by 21, to 44. SpaceX is the top-valued unicorn at $100 billion, contributing to a 40% increase in Ecosystem Value. Additionally, Los Angeles is home to NASA’s R&D center, the Jet Propulsion Laboratory, and Northrup Grumman's 110-acre campus. We have seen how universities contribute to an ecosystem, and LA hosts UCLA, CalTech, and USC. Nearly 1.5 million residents have a STEM degree.

Finally Tel Aviv, Israel, has seen a sharp increase in exits over $1 billion, with Fintech Pagaya having the highest exit in an IPO valued at $8.5 billion. Tel Aviv also had a 33-unicorn surge, increasing the total to 57, with Blockchain company Fireblocks as the highest-valued unicorn at $8.5 billion. The overall Ecosystem Value grew to $235 billion - up 100% from 2019H2 - 2021H2 to 2020H2 - 2022H2. Despite a globally challenging year for funding, startups in Israel raised $7 billion in 2023. Being a hub for global innovation centres, this is further exacerbated by moves such as the one in May 2023, when Tel Aviv University (TAU) launched an aggregation center for innovation. This was followed by the December 2023 announcement by the Israeli government of a $27.6 million initiative to establish nine innovation centers.

Now, the competition is stiff from both local and foreign startup ecosystems. Cost of living is exorbitant (56% higher in SV as compared to Austin). The high demand for top tech creates an over competitive hiring environment, overarching state regulation, and the high tax rates of California (CA ranks 48 out of 50 states in the State Business Tax Climate Index and the highest personal income tax rates for high-income individuals - 13.3%). This is creating an exodus of multiple startups and companies from SV to other locations in the United States like Austin, New York, and others. For instance, McAfee shifted its headquarters to Texas in 2023. Even Tesla founder Elon Musk admitted that there is a limit to which you can expand in the Bay Area, especially due to high living costs and long commute times, which motivated them to shift to Austin, Texas.

Yet, Silicon Valley continues to rally as the top performer in the index, accounting for 31% of the total value within the top 30 ecosystems. Among claims saying that Silicon Valley is losing its edge, a CrunchBase report finds that Silicon Valley still finds itself as an unparalleled ecosystem for startup development. It looks at this analysis through the lens of ‘scale-ups’, tech startups that have raised $1Mn since inception. Now, SV hosts 5x more scaleups than Israel, and about similar figures to the entirety of China and Europe. Locally, SV hosts 2.3x more scaleups than New York, 4.6x more than LA, and 8x more than Boston. As seen before, founders also find an open tap of investments in Silicon Valley as compared to counterparts. SV scaleups raised 2.6x more capital than the entirety of Europe and 1.1x as compared to China. Truly, SV’s risk-taking DNA sets it apart.

Networking and Community

No startup ecosystem is born by individual startups, individual companies, or individuals themselves. It is formed by the community’s collaborative involvement which helps in building the ethos and infusing the innovation in the ecosystem. And no doubt, SV, being one of the most influential ecosystems, has one of the most formidable communities, adorned with frequent networking events and massive tech and other sector-specific conferences, as well as community groups and industry associations.

Some popular networking events in SV are - Network AfterWork, IMPACT Hub, Startup Grind, ZURB’s Soapbox, Tech In Motion, 106 Miles, and General Assembly. These networking events provide great opportunities for founders, executives, and even students to connect with each other, opening a world of new avenues for each of them, while building their own communities.

SV also hosts multiple industry associations, such as the Silicon Valley Leadership Group, which was founded by David Packard (HP) in 1977, which today serves as a business association for the innovation economy of SV, with member companies like Airbnb, Amazon, and Adobe. SVLG, focusing on its Acceleration Agenda to develop Centres of Excellence(CoEs), recently launched initiatives to enhance diversity to 25% of leadership positions by 2025, enhance adoption of zero-emission vehicles, and increase investments into climate bonds. SV also has the SF Chamber of Commerce and SV Central Chamber of Commerce acting as pillars in this ecosystem.

Finally, Silicon Valley also hosts colossal conferences ranging across various target audiences. Some for example are the Developer Week (meant for developers), Startup Grind Global Conference (meant for entrepreneurs and others in the innovation business), Salesforce’s Dreamforce (meant for tech in general), the global TECHSPO SV (meant for tech in general), and TechCrunch Disrupt (which hosts the Startup Battlefield 200, a startup pitching competition). Many other names like Women Impact Tech, SaaS Connect, SaaStr, Cybersecurity and Cloud Congress, and ProductWorld adorn the decks of SV annually.

Conclusion

Silicon Valley, home to giants like Apple, Google, and Tesla, continues to thrive as a hub of innovation and entrepreneurial spirit, fostering the growth of disruptive startups. Silicon Valley remains pivotal in advancements across AI, biotech, cloud computing, and more, with OpenAI's $80Bn valuation exemplifying its innovative prowess.

With 11,811 startups and a staggering ecosystem value of $2.5Tn, Silicon Valley's growth rate of 10% contrasts with the global average of 46%, highlighting its maturity. The ecosystem's backbone includes venture capital, top-tier human capital, university-industry ties, government support, industrial structure, and a professional services network. Despite a dip in VC funding in 2022-2023, Silicon Valley still hosts 285 unicorns valued at $1,053.74Bn, underscoring its dominance.

Prominent VCs like Sequoia Capital, Andreessen Horowitz, and Accel have shaped the landscape, fueling AI startups and others. Support structures like Y-Combinator and initiatives from global governments bolster this ecosystem, ensuring its global appeal. Challenges like high living costs and competitive hiring are offset by a robust innovation economy, demonstrated by a high patent output and substantial government defence investments.

In conclusion, while Silicon Valley faces competition and evolving dynamics, its entrenched culture of risk-taking, extensive VC network, and unparalleled support structures ensure it remains the preeminent startup ecosystem, driving global technological advancement and innovation.

~Prabhav Agarwal